The SEC and CFTC have jointly proposed significant amendments to Form PF (Release No. IA-6959), the confidential reporting form that SEC-registered advisers to private funds are required to file. The proposal is the result of a comprehensive review of the form triggered by a January 2025 Presidential Memorandum directing agencies to evaluate and reduce regulatory burdens. For smaller private equity fund managers, the proposed changes are among the most consequential in Form PF’s history.

The headline change is straightforward: the SEC is proposing to raise the filing threshold for all Form PF filers from $150 million to $1 billion in private fund assets under management. If finalized, nearly half of current Form PF filers would no longer be required to file at all—a sweeping deregulatory step that would eliminate a meaningful compliance burden for emerging and smaller managers.

Background: What Form PF Requires Today

Form PF was adopted in 2011 pursuant to a Dodd-Frank Act mandate and requires SEC-registered advisers with $150 million or more in private fund assets under management to file confidential reports with the SEC. The data collected is used by the Financial Stability Oversight Council (FSOC) to assess systemic risk across the private fund industry.

For “small” private equity fund advisers (i.e. less than $2 billion in private equity fund AUM), Form PF filing currently involves completing Section 1 (general information about the adviser and its funds) and some of Section 4 (private equity-specific data including fund performance, borrowings, and investor composition).

What Would Change: The Filing Threshold

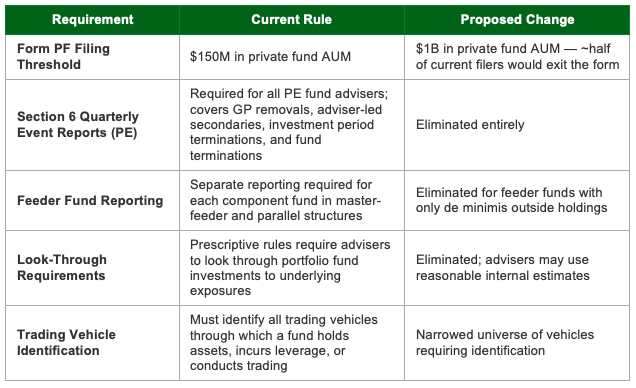

The most significant change for small private equity managers is the proposed increase to the Form PF filing threshold. The current threshold and the proposed threshold are compared below:

The SEC estimates that raising the threshold to $1 billion would eliminate filing obligations for approximately half of current Form PF filers, while still capturing over 90 percent of total private fund gross asset value reported on the form. The logic is sound: smaller advisers account for a disproportionately small share of overall assets, and their filing obligations impose costs that are not commensurate with their contribution to systemic risk data.

For a smaller private equity manager currently filing Form PF—particularly one advising funds in the $150 million to $999 million range—this change would mean a complete exit from Form PF obligations. No more annual filings, no Section 4 reporting, and no quarterly event reports under Section 6.

What Would Change: Elimination of Private Equity Quarterly Event Reporting

Beyond the filing threshold, the SEC is also proposing to eliminate Section 6 of Form PF entirely. Currently, all private equity fund advisers—regardless of AUM—are required to submit quarterly event reports covering:

- Adviser-led secondary transactions

- General partner removals or fund terminations initiated by limited partners

- Termination of investment periods

- Fund terminations

This is a significant development. Section 6 was added by the SEC’s 2023 amendments and was one of the more operationally intensive requirements for private equity advisers of all sizes. The SEC is now proposing to eliminate it in its entirety, acknowledging that the reporting imposes costs without sufficient corresponding benefit to FSOC’s systemic risk monitoring.

For smaller advisers that remain above the $1 billion filing threshold, elimination of Section 6 still represents a meaningful reduction in reporting burden. For smaller advisers that fall below the new threshold, this is moot—they will exit the form altogether.

Other Proposed Changes Relevant to Private Equity Advisers

Several additional proposed changes are worth noting for private equity managers that would remain Form PF filers under the new threshold:

- Feeder fund reporting: The proposal would eliminate separate reporting for feeder funds that hold only de minimis assets outside a single master fund, simplifying reporting for fund-of-fund and parallel fund structures.

- Look-through requirements: Current Form PF requires advisers to “look through” portfolio fund investments to identify underlying exposures. The proposal would eliminate prescriptive look-through requirements and allow advisers to use reasonable estimates consistent with their internal methodologies.

- Trading vehicle identification: The proposal would narrow the universe of trading vehicles that advisers must identify and report, reducing administrative overhead associated with complex fund structures.

Current vs. Proposed Requirements: Summary Comparison

The table below summarizes the key current requirements and proposed changes most relevant to private equity fund advisers:

What This Means in Practice

If the proposed amendments are finalized, the practical impact on smaller private equity managers falls into two categories.

Advisers below $1 billion in private fund AUM: You would no longer be required to file Form PF. This means no annual Form PF filing, no Section 4 private equity reporting, and no Section 6 quarterly event reports. For many smaller managers, this eliminates a meaningful and recurring compliance obligation. Keep in mind that this is a proposal—not a final rule—and advisers should continue to monitor the rulemaking for a final compliance date and any modifications.

Advisers above $1 billion in private fund AUM: You would still be required to file Form PF, but the elimination of Section 6 quarterly event reporting and the proposed streamlining of feeder fund, look-through, and trading vehicle requirements represent real reductions in reporting complexity. Advisers in this category should also note that the compliance date for the 2024 amendments remains October 1, 2026 pending finalization of this new proposal.

One important caveat: the SEC and CFTC are explicitly requesting comment on whether to modify private credit reporting requirements. Private equity managers with credit strategies or hybrid structures should watch this space carefully, as the SEC may impose new or revised requirements for private credit fund advisers as part of a future rulemaking.

How Trillium Can Help

Regulatory Change Preparedness: Trillium monitors proposed rules and translates them into clear, actionable assessments for your firm. As Form PF’s compliance framework evolves—including the outstanding October 2026 compliance date question—Trillium helps clients understand their specific obligations and prepare ahead of final rule adoption.

Compliance Program Support: For advisers that remain Form PF filers, Trillium provides hands-on support with Form PF preparation, Section 4 reporting, and ongoing monitoring of regulatory developments that affect your obligations.